As you may know or have figured out, I tend to use credit cards (especially signup bonuses) to earn most of my frequent flyer miles and points, earning close to a million since I started a little more than two years ago. Currently, I have 36 cards open (not so beautifully styled in the image above), though this number is constantly changing depending on my latest strategy.

Credit cards are one of my favorite things to talk about, and I’m going to be spending the next few weeks talking about the various cards on the market and what makes sense to get, but I thought I’d first answer some questions I commonly get asked having so many credit cards.

“Don’t all those credit cards hurt your credit score?”

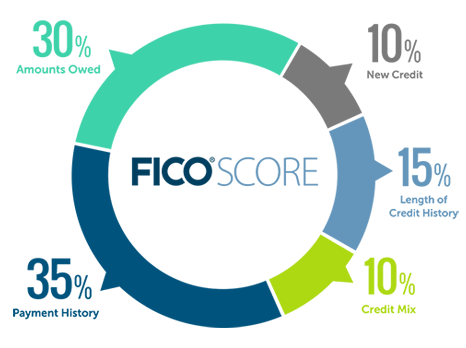

Not if you’re responsible. While the exact calculations are secret, FICO has disclosed the following approximations which go into calculating your credit score:

Photo courtesy of myfico.com

As you can see, “Payment History” is the most important. This is something that’s completely in your control, and is critically important. One late payment of 30 days or more can stay on your credit report for up to seven years, and can significantly affect your ability to obtain new credit (that being said, if you feel a late payment has been erroneously reported, you can file a dispute to have it removed). I have all of my cards set up to automatically deduct the new balance in full from my checking account every month so that I never have to worry about missed payments.

The next most important factor is “Amounts Owed.” For this, a calculation is performed to obtain what is known as your Debt-to-Income ratio, or DTI. This is a calculation of the balances on all your cards divided by the total credit on all your cards, the lower it is, the better it is for your score.. This is also where having many cards (or a few cards with very high limits) can be useful in raising your credit score. Because of all of the cards I have, my total credit available is somewhere in the range of $150,000. This means that if I’m carrying $1,000 worth of balances on my cards, my DTI is less than 1%. However, if you only have one card and it has a $5,000 limit, then you would have a DTI of 20%, lowering your credit score.

Next is length of credit history. This is the average length of credit card account. People like me tend to be a little lower here, since we are constantly opening up new accounts, though it is important to always keep your oldest accounts open, and never to cancel a card with no annual fee.

New credit is probably my worst area on this spectrum, as every time I apply for a new credit card, a hard inquiry is made on my report, causing my score to decrease slightly. Luckily, this is only worth 10%

The last one, credit mix, is also one of my generally lower-scoring areas. This measures the type of loans you have, and a more diverse set will yield a higher score. As credit cards represent my only type of “loans”, I generally don’t do well here. Again though, luckily it’s only 10%!

So as you can see, two-thirds of your credit score is based off of making your payments on time, and keeping your balances low in relation to total credit. Opening up lots of credit cards will not have an effect on these as long as you use your credit responsibly!

“So as long as I have a high credit score, I can get approved for any loan I want, even if I have a lot of credit card applications, right?”

No. Credit score is only one of several factors lenders use in determining whether to offer you a loan. No matter how good your credit score is, it’s going to look suspicious to a lender if you’ve made lots of recent applications for credit. The conventional wisdom says to avoid opening up any new credit cards for at least a year if you anticipate needing a loan for a large purchase like buying a house.

“But you must pay so much in annual fees! Is it really worth it?”

Actually, I don’t. I pay $100 in annual fees on my Citi Prestige card in order to make the points earned from it worth up to 60% more, and to get lounge access to over 700 lounges, as well as $85 on my Marriott Rewards card to get a free hotel night every year worth over twice that.

For almost any other card, there usually is no annual fee the first year, and then a fee the next year. When the annual fee hits the following year, I’ll first try to call up the issuer and ask them to waive the fee again (usually doesn’t work, but never hurts to try), and if that doesn’t work, I’ll then usually downgrade to another card with the same issuer that has no annual fee, allowing me to retain my credit history with that issuer (and avoid damaging my credit score). In certain situations where I can’t do this and the annual fee isn’t worth it, I will then cancel.

“Should I just cancel the card after the bonus hits?”

No. It doesn’t cost you anything to hold on to the card until the annual fee hits the next year, so you might as well keep it at least until the annual fee hits in order to increase your length of credit. The one exception to this might be cards with very high annual fees not waived the first year and very high bonuses, assuming the issuer will prorate the remainder of your annual fee. The one that comes to mind is the 100,000-point offer for the American Express Platinum, which also comes with a $450 fee the first year. If you hypothetically spend enough to hit this bonus in two months and don’t think the other benefits justify the high annual fee, you can cancel this card and receive $375 back (having only used it for one-sixth of a year).

“Your wallet must be huge! How do you lug all of those cards around!”

I don’t. Most cards are only good for the signup bonus; the ones I carry around with me on a daily basis are either ones on which I’m working towards a signup bonus, or ones that offer bonus rewards on certain categories (like dining out, gas, groceries, etc.)

“So what do you do with the rest of them?”

When I’m not creating beautiful collages for blog posts, I keep them in a drawer by my bed (and also use Google Sheets to store all the information so that I can still make an online purchase with one if I don’t have it physically with me).

“I have a crappy credit card with no good benefits that I opened up my freshman year of college which I never use anymore. Can I just get rid of it?”

Don’t. Given how important length of credit history is to your score, it’s costing you nothing to keep it open (while slowly improving your credit score each additional month it’s open), and will hurt your credit score severely if you close it (as your average age of account will become much younger).

“I’m going to be needing to put a large purchase on a card next month that I’ll probably pay off in 6-12 months. What’s a good card that I can open up to put this on so I can get a great bonus/rewards?”

Don’t do this. Credit card companies need to make money somehow, so it’s just not financially feasible for them to offer a card with great rewards and low interest rates. For example, there are many credit cards that offer bonuses of $400 or more after spending $3,000 in the first three months. If you plan on spending $3,000 in three months and paying it off in full at the end of each month, these are a great idea. If you’re planning on putting $3,000 on your card and paying it off progressively, these cards are a terrible idea, as they often tend to have APRs of 20% to 25%, meaning that the amount of interest you accrue on the debt would more than outweigh the bonus you receive. While I strongly strongly recommend paying off your balance in full every month, if you absolutely cannot, there are a number of 0% APR cards on the market that are better-served for this, though rewards will be minimal.

“How often should I open up new cards?”

If you’re pretty seriously into the credit card game, a general rule of thumb is to do a new round of applications every three months. This of course varies by issuer.

“I don’t want to risk opening up new cards unless there’s a good chance I’ll be approved. Is there anything I can do in advance?”

First, check directly with the issuers to see if there are any offers you’re prequalified for. Next, use the CardMatch tool on creditcards.com to see if there are any offers you’re prequalified for.

Lastly, if you know your approximate score (which you can obtain through Credit Sesame or Credit Karma) you can use the Creditpulls tool on CardBoards to find out the scores of other people who have been approved/denied for the card you want.

“This is too much for me to handle. Can’t I just open up one credit card and stick with it?”

Of course. It’s just a matter of if you want to be earning several hundred dollars in rewards a year (as you might with a 2% cashback credit card that you spent $1,000/month on), or several thousand (as you might if you’re constantly opening credit cards with signup bonuses worth several hundred).

“I don’t live in the US; is this really worth my time?”

Probably not. Credit card signup bonuses are far higher in the US than anywhere else in the world, primarily due to most Americans not being able to manage their debt well, meaning credit card companies are able to use those profits to offer extremely lucrative signup bonuses to those who do manage their debt well. This does present a bit of a moral quandary (i.e. is it wrong to cheer for people to manage their debt poorly so that signup bonuses stay high), but this is neither the time nor place to discuss this.

“What card should I open up in order to maximize X?”

Stay tuned.